Social Security was never designed as the main source of income for retirees but that is what it has become. Many older Americans simply did not prepare adequately. The taking away of pension plans was supposed to usher in the era of the self-directed 401k. One generation later the results are in and Americans are looking into the new retirement plan. The new retirement plan is working forever (in other words, until people can no longer physically hold down a job). This certainly doesn’t coincide with the brochures we see of older Americans galloping across the beach with cocktails in their hands.

The retirement savings crisis

Saving for retirement is flat out unsexy. Advertising is designed to separate Americans from their money even if it involves them going into massive levels of debt. Is it better to squirrel $500 a month away for 30 years in a boring index fund or is it better to lease a brand new shiny car? Most opt for the car. Also, with the median household income of $50,000 and the cost of living soaring, many Americans just don’t have money to set aside after all the bills are paid.

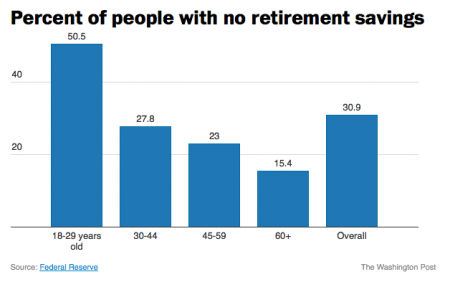

One scary fact is 30 percent of Americans flat out have zero dollars in retirement savings:

And according to Census data the typical American

household (bias by older families) has something like $17,000 to their

name when we remove housing equity. In other words, most Americans are

not prepared for a long retirement. And old age for many will be many

years. This is why you see many older Americans working deep into old

age. They simply need the money. Food costs are high. Housing costs

are high. And for this age group, healthcare costs are soaring.

Because of these changes people are pushing retirement age deeper into

the future.

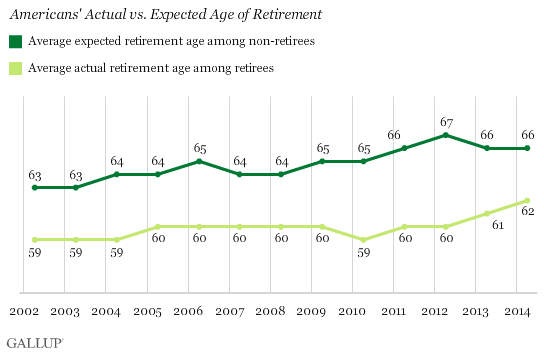

Average age of when people will retire and life predictionEven as the economy recovered, the average age of expected and actual retirement has jumped up:

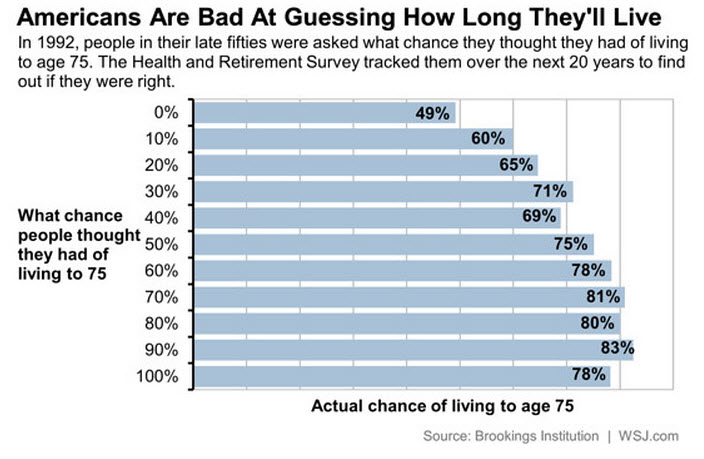

Americans are working more years than they once would have expected. Having a nest egg is crucial to being able to retire. And many Americans simply do not have adequate savings. Planning for the future is difficult. Many Americans are bad at planning how long they will live:

Retirement money held in the hands of the few

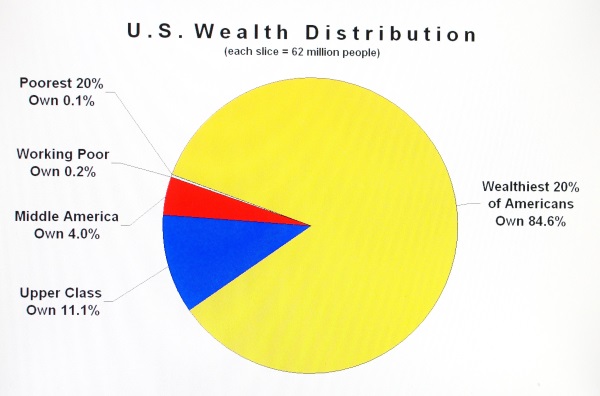

Half of Americans don’t own one stock. And the bulk of wealth is in the hands of a few. 84 percent of the nation’s wealth is held in the hands of the top 20 percent:

The rest whether they admit it or not, are going to

rely on Social Security. Most retired Americans rely on Social

Security as their primary source of income. Half of people on Social Security

would be out on the streets if it were not for their monthly payment.

As far as retirement planning goes, there very little retirement or

planning going on. And we have 10,000 Americans hitting retirement age

per day for the next decade.

No comments:

Post a Comment